By Abdul Shakoor

If a letter or robocall has ever told you that “this is your final notice from Cardholder Services” about lowering your credit card interest rate, you’ve brushed up against one of the longest-running scams in the financial world. It’s been around for years, it keeps mutating, and it works for one simple reason: it sounds just official enough to make a worried person pick up the phone.

The trick is in the name. “Cardholder Services” isn’t a company — it’s a deliberately vague, official-sounding label that could plausibly belong to your bank. That vagueness is the whole point. The scammers want you to assume it’s your card issuer without ever claiming to be a specific one, because naming a real bank would make the lie easier to catch. In this guide I’ll break down exactly how the scam works, the red flags that give it away, and what to do if a letter or call like this reaches you.

What the “Cardholder Services” scam actually is

At its core, this is a scam that impersonates a vague financial-services entity to trick you into handing over your credit card details, personal information, or an upfront fee.

It arrives in two main forms: a physical letter marked with urgent language (“Final Notice,” “Time Sensitive”), or a robocall with a recorded voice offering to “lower your interest rate.” Both funnel you toward the same goal — getting you on the phone with a live “agent” who then pressures you into revealing your card number, Social Security number, or paying a fee to “unlock” the lower rate that never actually existed.

The genius, if you can call it that, is that it preys on something real: lots of people genuinely do want lower interest rates. The scam dresses a universal wish up in official packaging and counts on urgency to override your caution.

📌 The trick is in the name: “Cardholder Services” isn’t a company. It’s a deliberately vague label that sounds like it could be your bank. Naming a real bank would make the lie easy to catch, so they stay vague on purpose and let you fill in the blank yourself.

The Scam at a Glance

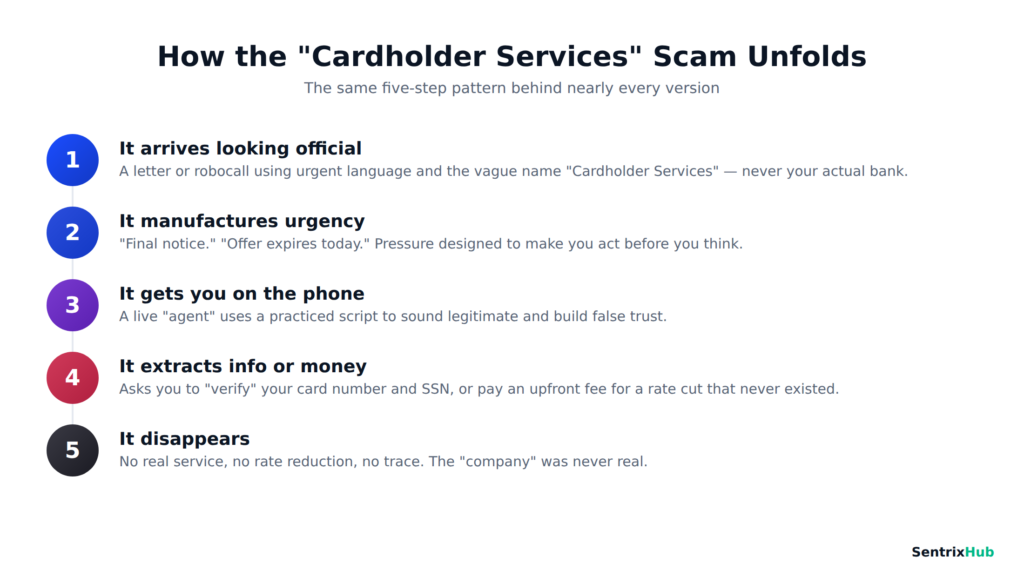

Before we break down each stage, here’s the whole scam in one view. Every version follows this same five-step arc — from the official-looking arrival to the disappearing act. Keep this shape in mind as we look at each step.

How the scam works, step by step

Once you see the sequence laid out, the manipulation becomes obvious.

It arrives looking official. The letter uses your name, official-looking fonts, a “notice” format, and urgent phrases. It rarely names your actual bank — just the generic “Cardholder Services.” A robocall version does the same job with a friendly recorded voice.

It manufactures urgency. “Final notice.” “Your eligibility is about to expire.” “Act now to lock in your reduced rate.” The pressure is deliberate — it’s designed to make you act before you think.

It gets you on the phone. The whole point is moving you to a live agent. Once you call, a real person uses a practiced script to sound legitimate and build false trust.

It extracts information or money. The agent asks you to “verify” your card number, expiry, security code, and often your Social Security number — or demands an upfront fee to process the rate reduction. Either way, you lose. They either drain the card, steal your identity, or take the fee and vanish.

It disappears. There’s no real service, no rate reduction, and no way to trace them. The “company” was never real.

Watch: The Scam in Action

If you’d like to hear what one of these calls actually sounds like, the video above breaks down the scam with real examples. Hearing the scripted urgency for yourself makes the red flags much easier to recognize the next time your phone rings.

The red flags that give it away

Every version of this scam carries the same tells. Any one of them should stop you cold.

The sender is vague — “Cardholder Services,” not the actual name of your bank. There’s artificial urgency — real financial institutions don’t threaten that a routine offer is about to expire in hours. They ask for sensitive details like your full card number, CVV, or Social Security number, which a legitimate issuer already has and would never cold-call to collect. There’s often an upfront fee to “secure” the lower rate — a legitimate rate reduction never works that way. And the offer is unsolicited: you never asked for this, yet here it is, marked “final notice.”

Put simply: your real bank knows who you are, already has your details, and doesn’t pressure you with countdown deadlines to hand them over again.

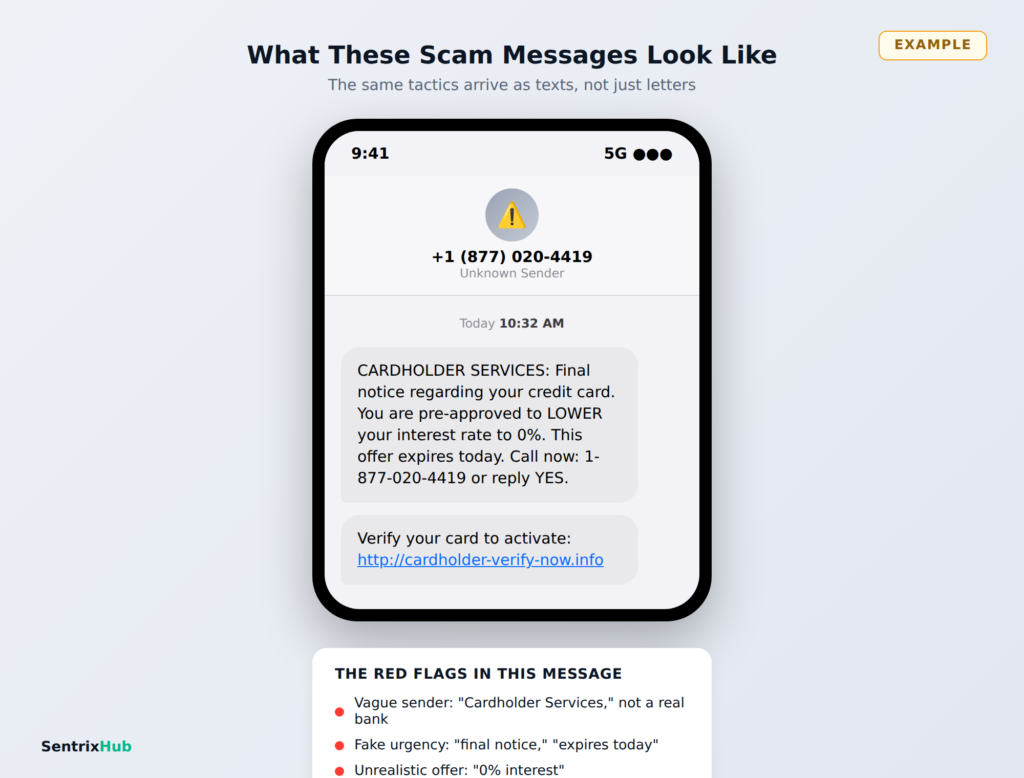

What These Scam Messages Look Like

These scams don’t only arrive as letters — the same tactics show up as text messages too. This example shows every red flag at once: a vague “Cardholder Services” sender, manufactured urgency, an unrealistic 0% offer, and a suspicious link. The format changes, but the manipulation is identical.

Why this scam refuses to die

You might wonder how something this old still works. The answer is that it evolves. The letters get more polished, the robocalls use better voice technology, and the scripts get sharper. It’s the same underlying deception you’ll recognize from other fraud patterns — the fake e-challan links that harvest OTPs or NADRA verification scams work on the identical principle: impersonate something official, manufacture urgency, and harvest what you hand over in a panic.

It survives because it costs almost nothing to send thousands of letters or place millions of robocalls, and it only needs a tiny fraction of people to bite. You don’t have to be careless to be targeted — you just have to be on a list.

What to do if you receive one

⚠️ Don’t press any button: On a robocall, pressing a key to “speak to an agent” or “be removed” just confirms your number is live and reaches a real scammer. That almost always means more calls, not fewer. Hang up instead.

The right response is refreshingly simple, and it comes down to not engaging.

Don’t call the number on the letter or press any button on the robocall — pressing a key just confirms your line is live and invites more calls. Never share card details, your SSN, or pay a fee to anyone who contacted you unexpectedly. If you’re genuinely curious whether your rate can be lowered, call your bank directly using the number printed on the back of your card — not any number the letter gave you. Report it: robocalls and mail fraud can be reported to the FTC (reportfraud.ftc.gov) and, for mailed versions, the US Postal Inspection Service. And if you did share anything, contact your bank immediately to freeze the card and watch for fraudulent charges.

The single most protective habit is the same one that defends against nearly every scam like this: treat any unsolicited contact asking for sensitive details as guilty until proven innocent, and verify through official channels you look up yourself.

✅ The golden rule: Your real bank already has your details and never cold-calls with a countdown deadline to collect them. If you want a lower rate, hang up and call the number on the back of your card yourself. Never trust a number the letter or call gave you.

Report It: The FTC Takes These Seriously

The FTC actively tracks these impersonation scams. Reporting yours at ReportFraud.ftc.gov feeds into investigations shared with thousands of law enforcers. It won’t resolve your individual case, but it helps authorities build cases against the operations behind these letters and calls — and it’s a reminder that scammers even impersonate the FTC itself.

The bigger lesson

The “Cardholder Services” scam is really a teaching example for a whole category of fraud. Strip away the specifics and the skeleton is always the same: an official-sounding but vague identity, a manufactured deadline, a request for sensitive data or money, and a disappearing act. Recognize that skeleton once, and you’ll spot it whether it arrives as a letter, a robocall, a text about a package, an email about your account, or even a questionable app you’re not sure you can trust. Good personal security — from healthy skepticism to strong, unique passwords and careful verification — is what keeps the whole family of these scams from ever getting a foothold.

You don’t need to memorize every scam. You just need to recognize the shape.

📌 Learn the shape, not every scam: Official-sounding but vague identity + a manufactured deadline + a request for sensitive data or money + a disappearing act. Once you recognize that skeleton, you’ll spot it as a letter, a call, a text, or an email.

Frequently asked questions

Is “Cardholder Services” a real company? No. It’s a deliberately vague, official-sounding label used by scammers so you’ll assume it’s your bank without them ever naming a specific, checkable institution.

What does the Cardholder Services scam want? Your credit card details, personal information (like your Social Security number), or an upfront fee to “lower your interest rate” — a service that doesn’t actually exist.

Is it safe to press a button on the robocall to be removed? No. Pressing any key simply confirms your number is active and reaches a real person, which usually leads to more calls, not fewer.

What should I do if I already gave them my card number? Contact your bank immediately using the number on the back of your card. Ask them to freeze or replace the card, and monitor your statements for unauthorized charges.

How do I report it? Report robocalls and fraud to the FTC at reportfraud.ftc.gov, and mailed versions to the US Postal Inspection Service. Reporting helps authorities track the operations.

How can I lower my interest rate for real? Call your card issuer directly using the number on your card and ask. A genuine rate reduction never requires an upfront fee or comes through an unsolicited “final notice.”

For more on spotting and avoiding fraud, see our guides on fake e-challan OTP scams, NADRA verification scams, and avoiding Cash App screenshot scams.

Abdul Shakoor writes practical, defensive cybersecurity and networking guides for SentrixHub. He focuses on making API security, mobile app security, authentication, and network concepts simple for beginners and developers.